Most barbershop and salon owners assume that buying an insurance policy checks the compliance box. It does not. State licensing boards, landlords, and local regulators each have their own requirements, and missing even one layer can trigger fines, license suspensions, or denied claims when you need coverage most. For owners managing multiple locations, the stakes multiply fast. This guide breaks down exactly what insurance compliance means in the salon and barbershop industry, which policies are legally required versus strongly recommended, how multi-location operations add complexity, and what a practical year-round compliance workflow looks like.

Table of Contents

- What insurance compliance really means for barbershops and salons

- Core insurance types required and recommended

- Multi-location compliance: licenses, insurance, and uniform standards

- Annual compliance tasks and optimizing coverage

- Why minimum state requirements are not enough

- Streamline your compliance with ShearShield

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Compliance is multi-layered | True compliance covers legal insurance, landlord demands, and licensing standards for every location. |

| Bundling saves money | Using business owners policies can cut insurance costs up to 30% while simplifying paperwork. |

| Annual review is essential | Policy audits and license checks each year prevent gaps, fines, and unplanned disruptions. |

| Minimums aren’t enough | Exceeding state requirements protects against risks landlords or boards might not anticipate. |

What insurance compliance really means for barbershops and salons

The word "compliance" gets thrown around loosely, but for salon and barbershop owners, it has a very specific meaning with multiple overlapping layers. It is not just about having a general liability policy on file. Insurance compliance for barbershops and salons involves maintaining all required insurance policies to satisfy state workers' compensation laws, landlord requirements, and licensing board standards, while also verifying individual practitioner licenses for every staff member across every location you operate.

Think of it as a three-layer system. The first layer is legal compliance, meaning the policies your state requires by law. The second is contractual compliance, meaning what your landlord or franchisor demands in your lease or agreement. The third is licensing compliance, meaning what your state cosmetology or barber board expects before they grant or renew your establishment license. Failing any one of these layers can have serious consequences.

Here is what many owners get wrong:

- Assuming that state licensing boards require liability insurance (many do not, but landlords almost always do)

- Forgetting to verify that individual stylist or barber licenses are current before adding someone to the floor

- Overlooking the difference between coverage for employees versus booth renters

- Missing the requirement to list landlords as additional insureds on the policy

"True compliance is not a one-time task. It is an ongoing process that touches licensing, insurance, and personnel records simultaneously."

The financial risk of non-compliance is real. Fines for operating without proper workers' compensation can reach tens of thousands of dollars in states like California and New York. A single denied insurance claim due to a lapsed policy or unlicensed staff member can cost far more than any premium savings. Using license compliance tools to track both insurance and licensing together is one of the most practical ways to close these gaps before they become expensive problems. For owners in California, reviewing California compliance guidance is a strong starting point given how detailed state requirements are there.

Core insurance types required and recommended

Once you understand what compliance covers, the next question is which policies you actually need. The answer depends on your state, your lease, and how your staff is classified. Here is a breakdown of the core policies and their typical annual cost ranges.

| Policy | Typical annual cost | Required or recommended |

|---|---|---|

| General Liability | $420 to $900 | Usually required by landlords |

| Professional Liability | $200 to $600 | Strongly recommended |

| Workers' Compensation | $0.52 to $3.00 per $100 payroll | Legally required in most states |

| Product Liability | $200 to $500 | Recommended for retail sellers |

| Business Owners Policy (BOP) | $500 to $1,500 | Recommended for bundling savings |

These cost benchmarks for salon insurance reflect national averages and can shift based on your state, payroll size, and claims history. A single-chair barbershop in a low-risk state will pay toward the lower end. A multi-stylist salon in a high-litigation state will pay more.

General Liability protects against third-party bodily injury and property damage claims. A client slipping on a wet floor, for example. Professional Liability, sometimes called errors and omissions, covers claims arising from the services themselves, like a chemical treatment that causes a scalp injury. These two are the foundation.

Workers' Compensation is where many owners get tripped up. It is legally required in most states the moment you hire your first W-2 employee, and the rate varies by job classification and payroll. Misclassifying a stylist as an independent contractor to avoid this cost is one of the most common and costly mistakes in the industry.

Pro Tip: If you sell retail products like shampoos or styling tools, make sure your general liability policy includes product liability coverage or add it separately. A client reaction to a product you sold can become a claim against your business.

The industry insurance guide recommends that most salon owners consider a Business Owners Policy as their baseline. A BOP bundles general liability and commercial property coverage into one package, typically at a lower combined cost than buying each separately. Managing all of these policies in one place through insurance policy management tools helps you track renewal dates and avoid coverage gaps.

Multi-location compliance: licenses, insurance, and uniform standards

Running two or more locations does not just double your workload. It multiplies the compliance variables in ways that catch many owners off guard. Each location is treated as a separate business entity by most state licensing boards and insurance carriers.

Owners must secure separate establishment licenses for each site, conduct premises inspections per location, and ensure uniform insurance coverage that often names landlords as additional insureds. This means your compliance checklist is not one list. It is one list per location.

Here is how the compliance requirements compare between a single location and a multi-location operation:

| Compliance task | Single location | Multi-location |

|---|---|---|

| Establishment license | 1 license | 1 per location |

| Premises inspection | 1 inspection | 1 per location |

| Workers' comp policy | 1 policy | May need separate or endorsed |

| Landlord additional insured | 1 landlord | 1 per lease agreement |

| Staff license verification | 1 roster | Separate roster per location |

For owners scaling from one to three or five locations, here is a practical sequence to follow:

- Apply for a new establishment license in the state or county where the new location will operate, well before your opening date.

- Schedule and pass the premises inspection required by your state board.

- Contact your insurance carrier to add the new location to your existing policy or issue a new policy, depending on carrier requirements.

- Collect certificates of insurance (COIs) naming each landlord as an additional insured.

- Verify that every stylist or barber working at the new location holds a current, valid license in that state.

"A license that is valid in Texas does not automatically transfer to a stylist working in your new Florida location. State reciprocity rules vary widely."

Booth renters add another layer. If a stylist rents a chair from you, they are typically responsible for their own professional liability insurance and their own license. However, your establishment license and general liability policy still cover the premises. Misunderstanding this distinction is a frequent compliance gap. Tools for managing multi-location compliance can help you maintain separate records for each site without losing track of who is covered where. Review state license requirements for each jurisdiction you operate in, because reciprocity and fee structures vary significantly.

Annual compliance tasks and optimizing coverage

Compliance is not something you set up once and forget. It requires a structured annual workflow to stay current, avoid penalties, and make sure your coverage actually reflects how your business operates today.

Here is a practical annual compliance checklist:

- Review all insurance policies at least 60 days before renewal to check for coverage gaps or outdated limits.

- Run a payroll audit for workers' compensation to make sure your reported payroll matches actual payroll. Underreporting triggers back premiums.

- Issue updated COIs to all landlords and any other parties who require them.

- Verify staff licenses for every employee and booth renter at every location. Pull license status directly from state board databases.

- Check establishment licenses to confirm renewal dates and submit applications before deadlines.

Annual policy reviews, payroll audits, COI issuance, and staff license verification are the core tasks that keep you compliant year-round. Bundling via a BOP can save 15 to 30% compared to buying policies separately, which adds up significantly across multiple locations.

Pro Tip: Set calendar reminders 90 days before every license and policy expiration date. Waiting until the renewal notice arrives in the mail is too late if your state board has a processing backlog.

Common pitfalls to avoid:

- Misclassifying booth renters as employees or vice versa, which affects workers' comp obligations

- Letting a single stylist's license lapse, which can jeopardize your establishment license in some states

- Failing to update your insurance carrier when you add a new service category like laser treatments or microblading

- Relying on spreadsheets that are not updated in real time

For California-specific workers' comp requirements, the rules are particularly strict, and fines for non-compliance are among the highest in the country. Using annual compliance tracking tools that automate reminders and centralize records is the most reliable way to stay ahead of these tasks across all your locations.

Why minimum state requirements are not enough

Here is an uncomfortable truth most compliance guides skip over: state licensing boards rarely require liability insurance as a condition of getting or keeping your establishment license. They care about sanitation, equipment standards, and practitioner credentials. Insurance is largely left to the market and your landlord.

That means an owner can be fully licensed and still be dangerously underinsured. We have seen this pattern repeatedly. A salon passes every inspection, holds every required license, and then faces a client lawsuit that wipes out years of profit because their liability limits were set at the state minimum from five years ago, before they added three chairs and doubled their revenue.

Experts recommend maintaining the full suite of insurance beyond minimum state mandates to guard against real-world risk. Landlord requirements are often the stronger driver of adequate coverage, but even those can lag behind what your actual exposure looks like.

Forward-thinking owners treat insurance compliance the same way they treat their best stylists: as an asset worth investing in properly. The minimum gets you in the door. The right coverage keeps you in business. Using advanced risk management tools helps you see the full picture across every location, so you are never caught relying on coverage that no longer fits.

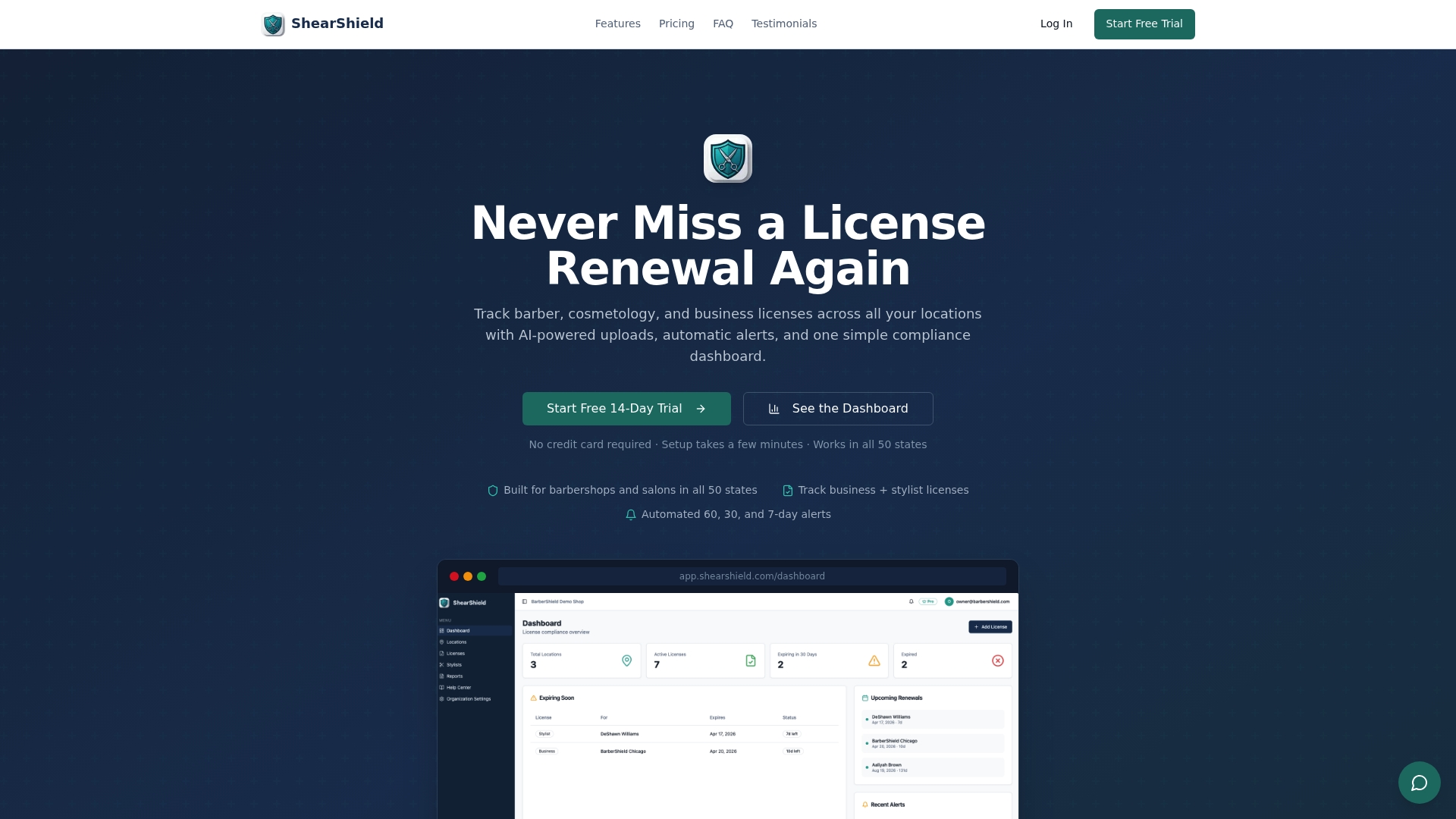

Streamline your compliance with ShearShield

Managing licenses and insurance across even two locations creates a real administrative burden. Tracking renewal dates, verifying staff credentials, issuing COIs, and staying current with state board changes is a full-time job layered on top of running your actual business.

ShearShield's dashboard was built specifically for multi-location barbershop and salon owners who need a centralized, automated way to handle all of it. The platform sends automated renewal alerts, stores license documents securely in the cloud, and gives you a real-time view of compliance status across every location. Instead of chasing spreadsheets, you get a single source of truth that keeps your team accountable and your business protected.

Frequently asked questions

What insurance is legally required for barbershops with employees?

Workers' compensation is legally required in most states as soon as you hire your first employee. General liability or professional liability may also be required by your landlord as a condition of your lease.

How do insurance requirements change when operating multiple salon locations?

Owners must secure separate establishment licenses and insurance policies for each location, meet individual landlord requirements, and often add each landlord as an additional insured on the relevant policy.

How can I reduce my insurance costs while staying compliant?

Bundling via a BOP saves 15 to 30% compared to purchasing general liability and commercial property separately, and reviewing policies annually prevents you from paying for outdated coverage.

What's the risk of misclassifying booth renters versus employees?

Booth renter misclassification can result in fines and retroactive workers' comp premiums, particularly in states like California where worker classification rules are strictly enforced.